Tax Benefits in Philanthropic Goal Planning

Want to make your charitable giving work harder for you? Smart planning can reduce your tax bill while maximizing the impact of your donations. Here’s what you need to know for 2026:

- New Tax Rules: Starting in 2026, itemized charitable deductions face a 0.5% AGI floor. For high earners, deductions are capped at 35%.

- Standard Deduction Changes: $16,100 for single filers, $32,200 for married couples. Non-itemizers can claim up to $1,000 ($2,000 for couples) for cash donations.

- Top Strategies: Use tools like Donor-Advised Funds (DAFs), Qualified Charitable Distributions (QCDs), and donate appreciated assets to maximize tax savings.

- Bunching Donations: Combine multiple years’ contributions into one tax year to exceed the standard deduction and unlock greater benefits.

The New "Hidden Floor" on Charitable Deductions Explained

sbb-itb-e723420

How Charitable Tax Deductions Work

Charitable tax deductions can be a useful way to align your giving with financial savings. Essentially, these deductions allow you to lower your taxable income when you donate to qualified organizations. By reducing your taxable income, you also reduce the amount of tax you owe. However, there are specific rules and documentation requirements you need to follow to claim these benefits.

Here's how it works: If you're in the 24% tax bracket and donate $10,000 to a qualified charity, you could lower your tax bill by $2,400. The exact savings depend on qualifying rules, deduction limits, and whether itemizing your deductions surpasses the standard deduction. Before counting on these benefits, make sure your donation meets IRS standards.

Who Qualifies for Charitable Deductions

Not all donations qualify for tax deductions. Only contributions to IRS-recognized organizations - such as 501(c)(3) nonprofits, religious groups, or government entities - are eligible [3][4]. Donations to individuals, political campaigns, or other non-qualified groups do not qualify, no matter how deserving the cause.

"A charitable contribution is voluntary, and is made without getting, or expecting to get, anything of equal value in return." – Taxpayer Advocate Service [5]

To ensure your donation qualifies, use the IRS Tax Exempt Organization Search (TEOS) tool to verify the organization’s status [3][4][6]. This simple step can save you from missing out on potential tax benefits.

Keep proper records: For cash donations, retain bank statements or receipts. If your donation is $250 or more, you'll need a written acknowledgment from the charity [3][6][7]. For non-cash donations over $5,000, a qualified appraisal and completion of Section B of Form 8283 are required [3][6][7].

If you receive something in return for your donation - like a ticket to a charity event - you can only deduct the amount that exceeds the fair market value of what you received. For instance, if you pay $500 for a charity dinner and the meal is valued at $100, only $400 is deductible [3][6].

Timing also plays a role. Donations must be made by December 31 of the tax year to count for that year’s deduction [5]. Cash donations to public charities are generally capped at 60% of your Adjusted Gross Income (AGI), while donations of appreciated assets held for over a year are limited to 30% of AGI [3][5][8]. If your contributions exceed these limits, the excess can be carried forward and deducted over the next five years [5][7].

Standard vs. Itemized Deductions

Taxpayers must choose between the standard deduction or itemizing their deductions on Schedule A - you can't do both [9]. For 2026, the standard deduction is set at $16,100 for single filers and $32,200 for married couples filing jointly [8][9].

Itemizing only makes sense if your total deductions exceed the standard deduction. These deductions can include charitable contributions, mortgage interest, state and local taxes (SALT), and medical expenses [9][8]. If your combined deductions are less than the standard amount, itemizing won't save you money.

Starting in 2026, new rules will apply. The "One Big Beautiful Bill Act" introduces a provision allowing taxpayers who take the standard deduction to claim up to $1,000 ($2,000 for married couples filing jointly) for cash donations to qualified charities [7]. This change provides a tax benefit for smaller donations without requiring itemization.

For itemizers in 2026, charitable contributions will only be deductible when they exceed 0.5% of AGI [8][7]. For example, if your AGI is $1 million, the first $5,000 in donations won’t provide an immediate tax benefit, although these amounts can be carried forward to future years [7]. Additionally, the tax benefit for itemized charitable deductions will be capped at 35%, even for those in the 37% tax bracket [8].

| Filing Status | 2026 Standard Deduction | Non-Itemizer Cash Deduction Limit |

|---|---|---|

| Single | $16,100 | $1,000 |

| Married Filing Jointly | $32,200 | $2,000 |

| Head of Household | $24,150 | $1,000 |

If your annual deductions are close to the standard deduction, you might consider "bunching" donations. This involves combining two years’ worth of charitable contributions into one tax year to exceed the standard deduction threshold. By doing so, you can make itemizing worthwhile and potentially increase your tax savings [8].

Strategies to Maximize Tax Benefits from Charitable Giving

You can amplify your tax savings and charitable contributions by using specific tax rules to your advantage. Below are some advanced techniques to help you make the most of your philanthropic efforts.

Donating Appreciated Assets to Avoid Capital Gains Tax

One powerful strategy is donating appreciated assets, like stocks or bonds, that you've held for more than a year. This approach lets you avoid capital gains tax while claiming a deduction for the asset's full fair market value - not just its original cost[10]. The result? A potentially larger tax benefit compared to selling the asset and donating the proceeds. For instance, if you donate $50,000 worth of stock with a $10,000 cost basis, you could receive a $17,500 tax deduction (at a 35% rate) and save about $9,520 in capital gains tax, totaling around $27,020 in benefits[11].

"When it comes to charitable giving, the benefits of donating appreciated securities are clear. Not only do donors receive a tax deduction for the full fair market value of the securities, but they also avoid capital gains tax on the appreciation." – Garrett Harbron, Head of Advised Wealth Management Strategies, Vanguard[12]

Interestingly, while 80% of donors own appreciated assets, only 21% donate them directly to charity[10]. By targeting assets with the highest appreciation, you can maximize your tax savings. Additionally, this strategy can help rebalance your portfolio. You can donate appreciated securities, use the cash you would have donated to repurchase the same securities, and reset their cost basis - all without triggering taxes.

Keep in mind that assets held for one year or less only qualify for a deduction at their cost basis, not their market value. For non-cash donations over $5,000 (except publicly traded stocks), you'll need a qualified appraisal and Form 8283. Deductions for long-term appreciated assets are capped at 30% of your adjusted gross income (AGI), but any excess can be carried forward for up to five years[10].

Using Donor-Advised Funds (DAFs)

Donor-Advised Funds (DAFs) are a flexible tool for charitable giving. They allow you to contribute assets, claim an immediate tax deduction, and decide later which charities will receive the funds. This is especially useful during high-income years - like before retirement or after selling a business - when offsetting income can make a big difference[16][17].

DAFs also make "bunching" donations easier. You can contribute a large sum to a DAF in one year, take the deduction, and then distribute the funds to charities over time at your convenience[13][14]. This eliminates the hassle of managing multiple receipts, as the DAF provides one consolidated tax receipt for all your contributions[17].

Here are some key details about DAFs:

- Cash contributions: Deduct up to 60% of your AGI.

- Appreciated assets: Deduct up to 30% of your AGI, with excess carried forward for five years[16][17].

- Minimum contributions: Typically range from $5,000 to $25,000, depending on the sponsoring organization[17].

- Additional benefits: No mandatory annual distributions and the option for anonymous grant-making[17].

However, contributions to a DAF are irrevocable. While you retain advisory privileges, the sponsoring organization legally owns the assets. Also, DAF funds can't be used for personal benefits, such as buying event tickets or fulfilling pledges[17].

Bunching Donations to Exceed the Standard Deduction

"Bunching" involves grouping several years' worth of charitable contributions into a single year to exceed the standard deduction threshold. In the "bunching year", you itemize your deductions to maximize savings, while in other years, you revert to the standard deduction[13][15].

This strategy works best for those whose itemizable deductions - like mortgage interest, state and local taxes (SALT), and charitable contributions - are close to the standard deduction. For 2026, the standard deduction is estimated at $16,100 for single filers and $32,200 for married couples filing jointly[15]. By consolidating two or three years of donations into one year, you can significantly increase your tax savings.

For example, at a 35% tax rate, bunching three years of $20,000 donations into one year could save $17,167.50 in taxes, compared to $9,502.50 if spread evenly over three years[15]. Over four years, this approach could result in $9,600 more in deductions for a couple with a $200,000 AGI[13].

Pairing bunching with a DAF offers even greater benefits, including an immediate deduction at fair market value, capital gains tax avoidance, and tax-free growth of assets within the DAF[13]. To get started, calculate your itemizable expenses to see how close you are to the standard deduction. If you're within range, bunching could unlock substantial tax savings while ensuring steady support for your favorite causes.

Tax Planning Tools for Charitable Giving

Smart tax planning can simplify charitable giving, turning what might feel like a logistical headache into a smooth process that ensures you maximize your tax benefits. Whether you're managing distributions from retirement accounts or keeping track of smaller, everyday donations, the right tools can help you get every eligible deduction while staying on the right side of IRS rules.

Qualified Charitable Distributions (QCDs) from IRAs

If you're 70½ or older, a Qualified Charitable Distribution (QCD) is a powerful way to give. It allows you to transfer up to $111,000 (2026 limit) directly from a traditional IRA to a 501(c)(3) charity. The best part? That amount is excluded from your taxable income, making IRAs a great choice for charitable donations [2].

The key here is that the funds must go straight from your IRA custodian to the charity. If you withdraw the money first, it becomes taxable income. When filing your taxes, report the total distribution on Form 1040, Line 4a, and the taxable portion (after subtracting the QCD) on Line 4b, noting "QCD." It's a good idea to complete your QCDs early in the year or before taking your Required Minimum Distributions (RMDs).

There’s also a one-time lifetime option to transfer up to $55,000 from an IRA to a charitable remainder trust or charitable gift annuity. However, keep in mind that QCDs cannot go to Donor-Advised Funds, private foundations, or supporting organizations. Beyond lowering taxable income, QCDs can reduce the taxation of Social Security benefits, lower Medicare premiums, and help you qualify for other income-based tax breaks. To ensure your donation qualifies, verify the charity’s 501(c)(3) status using the IRS Tax Exempt Organization Search. This approach not only reduces your tax burden but also ties seamlessly into your broader charitable goals.

Using Deductible.me for Tax-Optimized Giving

For everyday donations, tools like Deductible.me make tracking and documenting contributions much easier. This app is particularly helpful for non-cash donations like clothing, furniture, and household items. It uses researched fair market values to automate the valuation of goods in good used condition. It also tracks volunteer expenses, including mileage (at 14 cents per mile), and generates IRS-compliant reports - minimizing paperwork hassles while keeping you compliant.

The app is especially useful for managing documentation thresholds. For example:

- Donations of $250 or more require a contemporaneous written acknowledgment.

- Non-cash contributions exceeding $500 need Form 8283.

- Items or groups of similar items valued over $5,000 require a professional appraisal.

As FindCPA points out:

"The Tax Court has repeatedly upheld disallowance even where the taxpayer clearly made the gift and the valuation was reasonable, simply because the paperwork was deficient."

Deductible.me simplifies this process by producing IRS-ready reports that organize your annual donations. This becomes even more important in 2026 with the introduction of a 0.5% AGI floor on itemized charitable deductions.

For casual donors, the free plan tracks up to $500 in donation value and includes AI photo scanning and basic receipt management. The Premium plan, priced at $2/month, offers unlimited tracking, advanced analytics, annual giving goal monitoring, and priority support. It also helps you determine if your itemized deductions exceed the 2026 standard deduction of $16,100 for single filers or $32,200 for joint filers. By automating valuation and documentation, Deductible.me ensures you capture every eligible deduction and align your everyday giving with your overall tax strategy.

Adjusting Charitable Strategies for Tax Law Changes

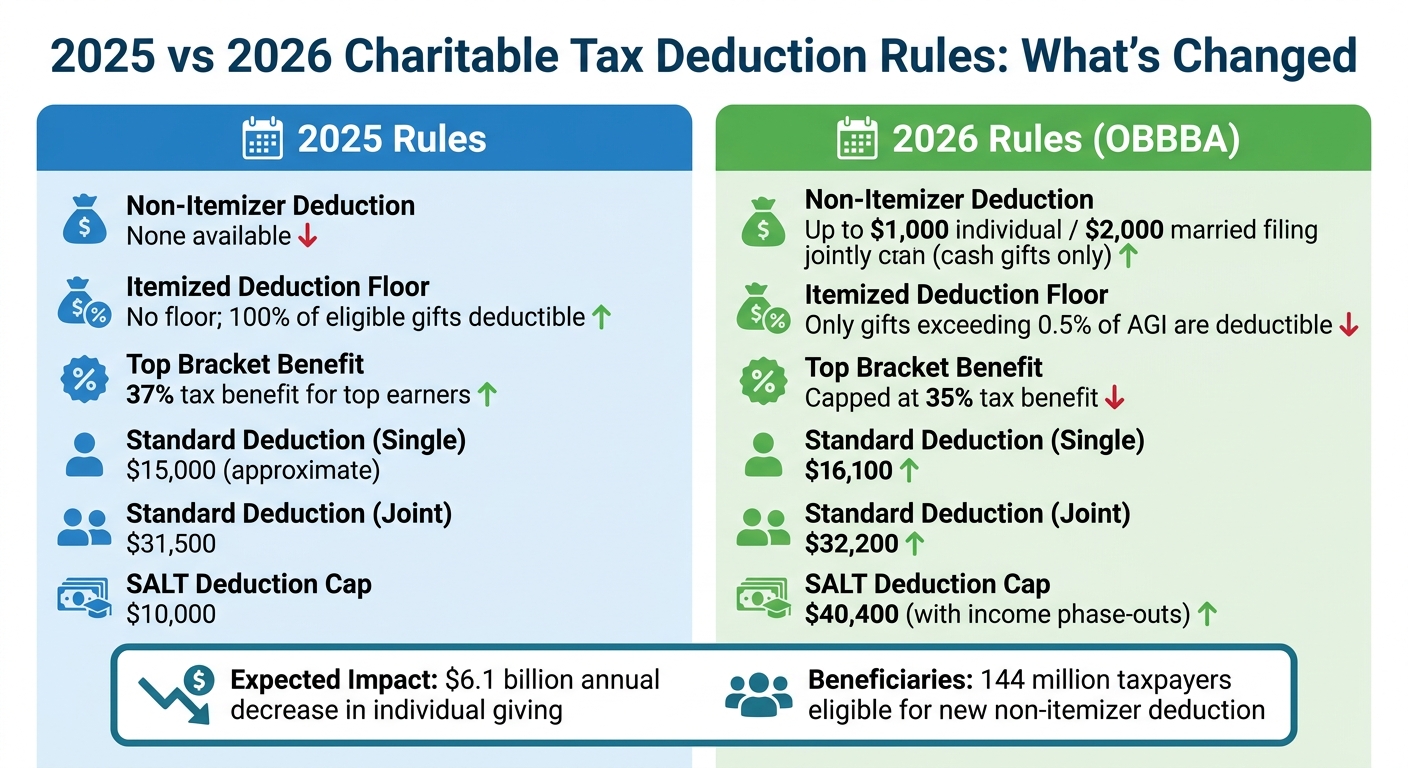

2025 vs 2026 Charitable Tax Deduction Rules Comparison

How 2026 Tax Changes Will Affect Charitable Giving

The charitable giving landscape has shifted significantly with the implementation of the One Big Beautiful Bill Act (OBBBA) on July 4, 2025. Starting in 2026, donors will face both new opportunities and challenges when planning their contributions [22][23].

One of the most notable changes is the introduction of a 0.5% Adjusted Gross Income (AGI) floor for itemizers. This means that to qualify for tax benefits, your charitable donations must exceed 0.5% of your AGI [22]. For example, if your AGI is $300,000, the first $1,500 of your donations won't provide any tax advantage due to this new threshold [22].

"This significant change effectively eliminates the tax benefit of smaller, routine donations"

– Kate Schubel, Tax Writer at Kiplinger [18]

High-income taxpayers will also see a reduction in the benefits they receive. Those in the top 37% tax bracket will now only receive a 35% deduction on their charitable contributions, which can significantly impact larger gifts. This adjustment is expected to decrease individual giving by $6.1 billion annually [20][22].

On the brighter side, taxpayers who take the standard deduction - roughly 90% of Americans - can now claim an above-the-line deduction for cash donations. Individuals can deduct up to $1,000, while married couples filing jointly can deduct up to $2,000 [22]. However, this applies exclusively to cash gifts (e.g., donations via check, credit card, or payroll deduction) made to qualified 501(c)(3) organizations. An estimated 144 million taxpayers could benefit from this new provision [18].

The standard deduction itself has increased to $16,100 for single filers and $32,200 for joint filers in 2026, making it less likely for many taxpayers to itemize [22]. However, the SALT (State and Local Tax) deduction cap has risen to $40,400, which may encourage some to reconsider itemizing [22].

These updates make strategies like bunching donations and using Qualified Charitable Distributions (QCDs) even more essential for effective tax planning, as discussed earlier.

Preparing for Future Tax Scenarios

Adapting your charitable giving strategy to these new tax rules is key. One popular method is bunching, where you consolidate several years' worth of donations into a single year. This approach can help you surpass both the higher standard deduction and the new 0.5% AGI floor [22].

"A bunching strategy or an approach of making larger gifts with less frequency can be more effective under the new rules"

– Fidelity Charitable [22]

For taxpayers aged 70½ or older, Qualified Charitable Distributions (QCDs) remain an excellent way to give directly from an IRA while enjoying tax benefits.

"The new tax law has made IRA giving more advantageous for taxpayers over the age of 70 ½"

– Professor Christopher Hoyt, University of Missouri School of Law [21]

Timing is another critical factor. If you plan to itemize, calculate your 0.5% AGI threshold early in the year to understand how much you need to donate before additional contributions become deductible [19]. For those taking the standard deduction, aim to give at least $1,000 (or $2,000 if married) in cash to maximize the above-the-line deduction [18].

"Under the 2026 rules, planning throughout the year may offer greater tax savings and clearer alignment with your long-term charitable goals"

– Cheri Dorsey, Attorney at Sessa & Dorsey [19]

| Feature | 2025 Rules | 2026 Rules (OBBBA) |

|---|---|---|

| Non-Itemizer Deduction | None | Up to $1,000 ($2,000 joint) for cash gifts |

| Itemized Deduction Floor | No floor; 100% of eligible gifts deductible | Only gifts exceeding 0.5% of AGI are deductible |

| Top Bracket Benefit | 37% tax benefit for top earners | Capped at 35% tax benefit |

| Standard Deduction (Joint) | $31,500 | $32,200 |

| SALT Deduction Cap | $10,000 | $40,400 (with income phase-outs) |

These tax updates highlight the importance of proactive planning to ensure your charitable giving aligns with your financial goals and maximizes available benefits.

Conclusion: Aligning Philanthropy with Financial Goals

Strategic charitable giving isn’t just about supporting causes - it’s about weaving philanthropy into your financial plan to amplify both its impact and tax benefits. With billions donated each year, fine-tuning your approach can make a big difference.

The foundation of effective giving lies in adopting a total net worth approach. This means looking at how tools like donor-advised funds (DAFs) and Qualified Charitable Distributions (QCDs) complement your broader financial strategy. For example, you might secure deductions during peak income years, use QCDs to meet Required Minimum Distributions (RMDs), or donate appreciated securities to sidestep capital gains taxes. Each of these methods should align seamlessly with your financial goals.

"Charitable giving is most effective when it is aligned with your overall financial strategy... evaluating charitable opportunities within the broader context of their finances including cash flow, tax planning strategies, investments, estate planning strategies, and long-term goals."

– Kenneth J. Dean, CPA, CFP®, CFA, MST, Winthrop Wealth [1]

Tools like Deductible.me streamline the process by offering AI-powered valuations for donated items, IRS-compliant reporting, and tracking features to help you stay on top of your giving goals. With tax changes on the horizon - like the 2026 introduction of a 0.5% AGI floor and new above-the-line deductions for non-itemizers - having accurate documentation and strategic tools is more important than ever to maximize your tax savings.

FAQs

Will the 0.5% AGI floor limit my deduction if I give small amounts?

Starting in 2026, only charitable donations that exceed 0.5% of your adjusted gross income (AGI) will be eligible for tax deductions. Contributions below this threshold won’t qualify. To make the most of your tax benefits, consider planning your donations carefully and ensuring they meet or surpass this limit.

Which is better for taxes: donating cash, appreciated stock, or using a DAF?

Donating stocks or securities that have increased in value and been held for over a year can offer more tax advantages than giving cash. Why? It helps you sidestep capital gains taxes while also letting you deduct the full market value of the donation. Using a Donor-Advised Fund (DAF) takes this a step further by offering a mix of immediate tax deductions, tax-free growth on the assets, and the flexibility to decide on charitable contributions over time. While cash donations are straightforward, they might lead to higher taxes if you have appreciated assets you could donate instead.

How can I keep IRS-proof donation records all year?

To ensure your donation records are ready for the IRS, it's important to keep detailed documentation for every charitable contribution. This includes receipts that clearly show the organization’s name, the donation date, a description of the contribution, and the amount.

For better organization, consider using a reliable tracking system or app to log donations consistently throughout the year. If you're donating non-cash items, make sure to accurately value these contributions and keep any supporting documents, such as appraisals or receipts, as proof.

By regularly updating and reviewing your records, you'll stay prepared and compliant when it’s time to file your taxes.