IRS Rules for Non-Cash Donations

Non-cash donations, like clothing, furniture, or stocks, can reduce your taxable income if you follow IRS rules. To claim deductions:

- Donate to IRS-recognized charities (e.g., 501(c)(3) organizations).

- Determine the fair market value (FMV) of donated items, based on current resale value, not purchase price.

- Ensure items like household goods are in good used condition or better unless valued over $500 with an appraisal.

- Itemize deductions on Schedule A of Form 1040 if your total itemized deductions exceed the standard deduction.

- Use Form 8283 for non-cash donations exceeding $500 and attach appraisals for items worth over $5,000.

Accurate documentation is key. Missing receipts, incomplete forms, or overvaluing donations can lead to penalties or denied deductions. Always keep detailed records, including photos, written acknowledgments, and appraisals, to ensure compliance.

For donations under $250, a receipt suffices. Contributions over $250 need a written acknowledgment. Donations over $5,000 require both an appraisal and charity signatures on Form 8283. Follow these steps to maximize your tax benefits while staying compliant.

How Do I Deduct Non-cash Charitable Donations? - Tax and Accounting Coach

sbb-itb-e723420

What Qualifies as a Non-Cash Donation

A non-cash donation refers to any property given to a qualified charity, ranging from everyday items like clothing to financial assets such as stocks or real estate [2].

Types of Non-Cash Donations That Qualify

The IRS permits deductions for various types of donated property, provided they meet specific criteria. For instance, household goods like clothing, furniture, electronics, appliances, and linens must be in "good used condition or better" to qualify [2]. Beyond household items, other eligible donations include:

| Category | Examples |

|---|---|

| Financial assets | Stocks, bonds, mutual funds |

| Vehicles | Cars, boats, aircraft |

| Specialty items | Jewelry, art, collectibles |

| Other property | Real estate, patents, business inventory |

For publicly traded securities, the contribution is considered made on the date the endorsed certificate is delivered or the transfer is recorded on the corporation's books [2].

Items That Do Not Qualify

Not all property contributions are eligible for tax deductions. For example, donating your time or professional services - even if you volunteer in your professional field - does not qualify since the value of labor is not considered property [3]. Similarly, contributions made to individuals, political organizations, or groups not recognized as qualified charitable organizations by the IRS are ineligible. Most foreign organizations are also excluded unless they fall under specific tax treaties [3].

"You cannot take an income tax charitable contribution deduction for household items unless they are in good used condition or better." - IRS Publication 561 [2]

One exception applies to household items in poor condition valued at over $500. In such cases, you can claim a deduction if you obtain a qualified appraisal and submit Form 8283 with your tax return [2]. However, items in poor condition valued under $500 are not deductible. Next, we’ll discuss who is eligible to claim these deductions.

Who Can Deduct Non-Cash Donations

When it comes to non-cash donations, not every taxpayer can claim a deduction. The IRS has specific rules about which contributions qualify and what documentation is necessary to stay compliant.

Donating to IRS-Recognized Organizations

To qualify for a deduction, your donation must be made to an organization recognized by the IRS under section 170(c) of the Internal Revenue Code. These include:

- 501(c)(3) nonprofits

- Churches and religious organizations

- Government entities (if the donation serves a public purpose)

- Veterans' organizations

- Nonprofit volunteer fire companies [3]

However, donations made directly to individuals are not deductible [1]. If you're unsure about an organization's status, you can use the IRS Tax Exempt Organization Search tool on IRS.gov. This tool also shows the applicable adjusted gross income (AGI) deduction limits - typically 50% for public charities and 30% for certain private foundations and fraternal societies [3]. The next step is understanding how to itemize deductions to claim these contributions.

Itemizing Deductions on Schedule A

To deduct non-cash donations, you must itemize your deductions on Schedule A of Form 1040 instead of taking the standard deduction [3][1]. This means your total itemized deductions must exceed the standard deduction for your filing status to benefit from any charitable contributions.

"Currently, you can only deduct charitable contributions if you itemize deductions on Schedule A (Form 1040), Itemized Deductions... Beginning with tax year 2026, if you do not itemize, you may deduct up to $1,000 ($2,000 if filing jointly) of your cash contributions to certain qualified organizations." - Internal Revenue Service [1]

It’s important to note that the above-the-line cash deduction available starting in tax year 2026 does not apply to non-cash donations [1]. Another key factor to consider is how receiving benefits in return for your donation impacts the deduction amount.

Partial Benefits and Quid Pro Quo Contributions

If you receive any benefit in return for your donation, the IRS requires you to deduct only the amount that exceeds the fair market value of the benefit you received.

"If you receive a benefit in exchange for the contribution... you can only deduct the amount that exceeds the fair market value of the benefit received or expected to be received." - Internal Revenue Service [1]

For example, if you pay $300 to attend a charity gala and the dinner provided is valued at $75, the deductible portion of your contribution is $225. Additionally, charities must provide a written disclosure for any quid pro quo contribution over $75. Failure to do so can result in penalties of $10 per contribution, up to $5,000 per fundraising event [5]. Keeping detailed records of these transactions is crucial to ensure compliance with IRS requirements.

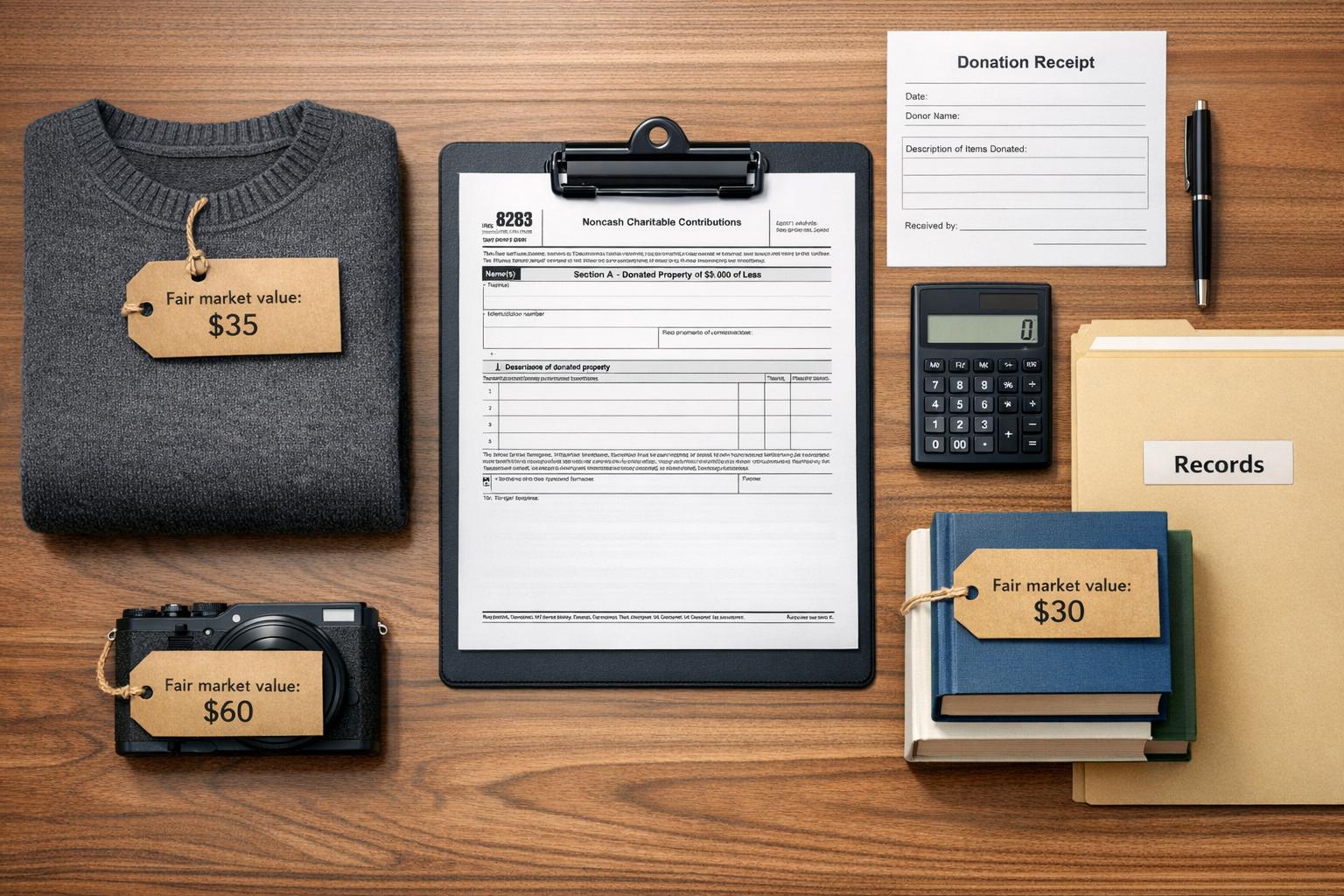

How to Value Non-Cash Donations

IRS Non-Cash Donation Thresholds: Documentation & Form Requirements

Accurately valuing your non-cash donations is essential if you want to claim a deduction. The IRS specifies that non-cash donations must be valued at their fair market value (FMV) on the date of the donation - not what you originally paid for the item.

Fair Market Value and Item Condition

"FMV is the price that property would sell for on the open market. It is the price agreed upon by a willing buyer and seller, both fully informed." - IRS Publication 561 [2]

In simple terms, this means figuring out what the item would realistically sell for today. For items like clothing or household goods, this often involves checking resale or thrift store prices. The condition of the item plays a big role here - a gently used couch will have a higher FMV than one that’s heavily worn. For publicly traded stock, FMV is calculated as the average of its high and low trading prices on the date of the donation [2]. Always document the condition of your items with clear photographs.

Once you’ve determined the FMV, it’s time to review the IRS thresholds to ensure you meet the necessary documentation requirements.

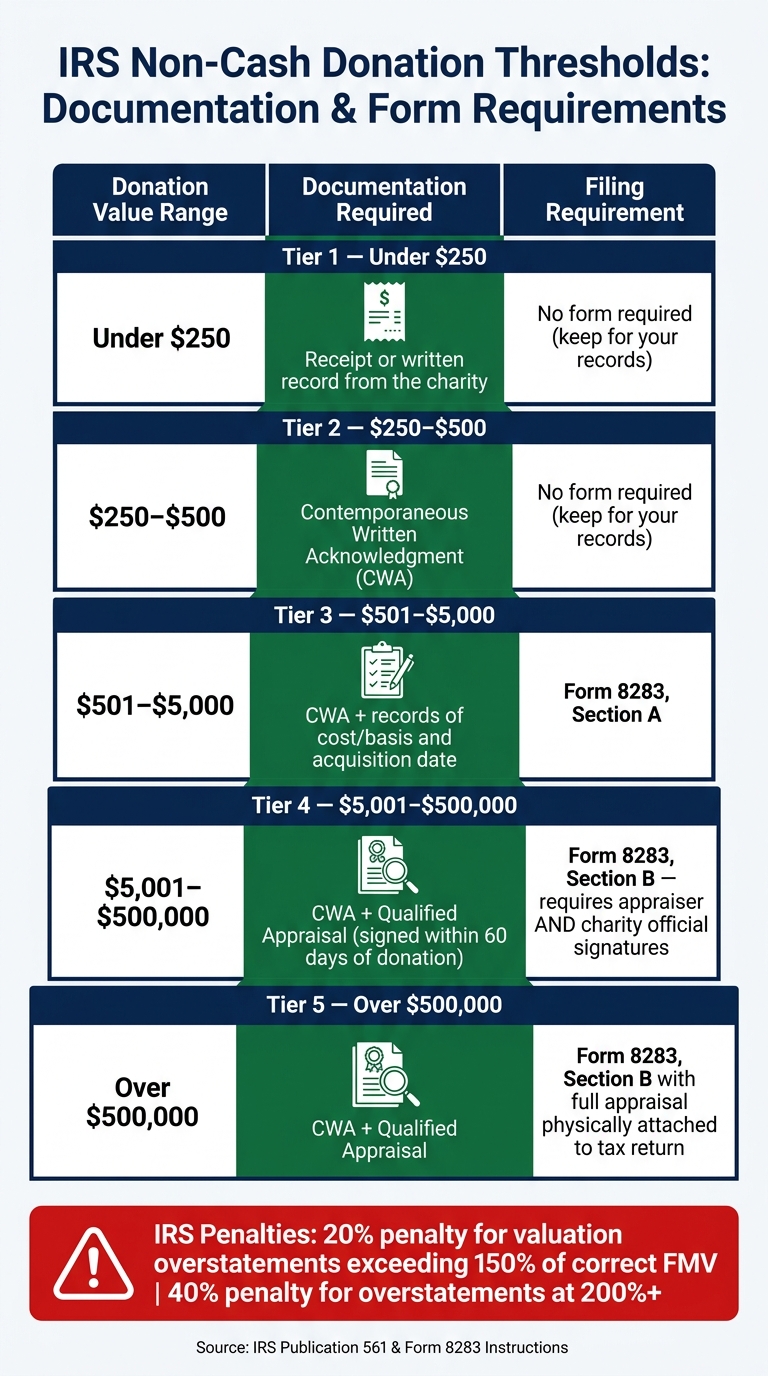

IRS Valuation Thresholds

The IRS has specific documentation requirements based on the value of your donation. Here’s a quick breakdown:

| Donation Value | Documentation Required | Filing Requirement |

|---|---|---|

| Under $250 | Receipt or written record from the charity | None (keep for your records) |

| $250–$500 | Contemporaneous Written Acknowledgment (CWA) | None (keep for your records) |

| Over $500–$5,000 | CWA plus records of cost/basis and acquisition date | Form 8283, Section A |

| Over $5,000 | CWA plus qualified appraisal | Form 8283, Section B (requires appraiser and charity signatures) |

| Over $500,000 | CWA plus qualified appraisal | Form 8283, Section B with the appraisal physically attached to the return |

These thresholds are based on IRS guidelines [2][6].

Special Rules to Keep in Mind

The IRS has additional rules for grouping similar items. If you donate similar items throughout the year - like books, clothing, or furniture - you must combine their values when determining whether you’ve crossed the $5,000 threshold. For instance, if you donate books worth $3,000 to one charity and $2,500 to another, the total exceeds $5,000, so you’ll need a qualified appraisal [6].

Donations of art come with even stricter guidelines. If you’re claiming a deduction of $20,000 or more, a signed appraisal must be included with your return. For pieces valued at $50,000 or more, you can request a formal "Statement of Value" from the IRS before filing [2]. Any appraisal must be dated within 60 days before the donation date [6].

Understanding these rules and documenting your donations properly can help you avoid issues when filing your taxes.

IRS Forms and Records Required for Non-Cash Donations

Once you've determined the fair market value of your non-cash donation, the next step is to ensure you have the right IRS forms and records. The IRS has detailed requirements, and missing even one document could jeopardize your deduction.

Form 8283 and Appraisal Requirements

Form 8283 (Noncash Charitable Contributions) is the key document for reporting non-cash donations. If your total non-cash contributions for the year exceed $500, you must include this form with your tax return [6].

The form is divided into two sections, and the section you complete depends on the value of your donation:

| Donation Value | Form 8283 Section | Qualified Appraisal Required? | Signatures Required? |

|---|---|---|---|

| $501–$5,000 | Section A | No | No |

| Publicly traded stock (any value) | Section A | No | No |

| Single item or similar group over $5,000 | Section B | Yes | Appraiser + charity official |

| Single item over $500,000 | Section B | Yes (attach full appraisal to return) | Appraiser + charity official |

For donations requiring Section B, you’ll need a qualified appraisal signed and dated within 60 days of the donation. Additionally, Section B mandates signatures from both the appraiser and an authorized official from the charity.

"The signature [on Form 8283] does not represent agreement with the appraised value of the contributed property. A signed acknowledgement represents receipt of the property described." - IRS [7]

If you're donating a vehicle valued at over $500, you'll also need to attach Form 1098-C or an equivalent written acknowledgment. Keep in mind that for vehicles, your deduction is capped at the amount the charity earns from selling the vehicle [6].

Properly completing Form 8283 and securing appraisals ensures compliance with IRS requirements and supports your deduction claim.

Written Acknowledgments from Charities

In addition to appraisals, you’ll need written documentation from the charity. For donations of $250 or more, the IRS requires a Contemporaneous Written Acknowledgment (CWA). This acknowledgment is a must-have for claiming your deduction.

"The donor is responsible for requesting and obtaining the written acknowledgement from the donee." - Internal Revenue Service [5]

A valid CWA must include:

- A description of the donated property.

- A statement indicating whether the charity provided any goods or services in return.

- A good faith estimate of the value of any goods or services provided, if applicable.

You must receive this acknowledgment before filing your return or by the return's due date (including extensions) - whichever comes first [6].

For additional transparency, if the charity sells or disposes of your donated property within three years, they are required to file Form 8282 and send you a copy [7]. This creates a clear paper trail for the IRS to verify your original deduction.

Proper forms and records, including appraisals and written acknowledgments, are essential to ensure your non-cash donations meet IRS standards.

IRS Rules Specific to Household Item Donations

Donating household items - like furniture, appliances, electronics, and clothing - comes with specific IRS guidelines. Understanding these rules can help ensure your deductions are accepted.

Condition Standards for Donated Household Items

The IRS categorizes household items as furniture, furnishings, electronics, appliances, and linens. However, paintings, antiques, jewelry, gems, and collections are not included in this category and are subject to separate rules [2][8].

For items that do fall under the household category, the IRS has a clear standard:

"You cannot take an income tax charitable contribution deduction for household items unless they are in good used condition or better." - IRS Publication 561 [2]

A simple rule of thumb: if you’d feel comfortable giving the item to a friend, it likely meets the standard.

Exception: If an item is not in good used condition but has a claimed value over $500, you must include a qualified appraisal and complete Form 8283 (Section B) [2][8].

Also, keep in mind that used household items typically have a much lower value than their original purchase price:

"The FMV of used household items is usually much lower than the price paid when new... Such used property may have little or no market value because it may be out of style." - IRS Publication 561 [2]

When estimating the fair market value (FMV), consider what the item would sell for at a thrift store or consignment shop - not its original retail or replacement cost [2][4].

In addition to ensuring the condition of your items, proper documentation is essential to meet IRS requirements.

What Records to Keep for Household Donations

The documentation you need depends on the value of your donation. Here’s how it breaks down for household items:

| Donation Value | Required Documentation |

|---|---|

| Less than $250 | Receipt from the charity, including the name, date, and a description of the item. If a receipt isn’t practical (e.g., using a drop box), keep your own written record of FMV and condition [9]. |

| $250–$500 | Contemporaneous Written Acknowledgment (CWA) from the charity [9]. |

| $501–$5,000 | CWA and Form 8283, Section A [1][9]. |

| Over $5,000 | CWA, a qualified appraisal, and Form 8283, Section B [1][9]. |

To strengthen your records, photograph each item before donating. These photos can be crucial if the IRS audits your deduction [4]. For higher-value items, check recent sales of similar items to confirm FMV [4].

Finally, if you’re donating at an unattended drop-off point, maintain a written log that includes the charity’s name, the date, a description of the items, their FMV, and their condition [9].

Common IRS Compliance Mistakes to Avoid

When it comes to securing your deductions, understanding proper valuation and documentation practices is just the beginning. Avoid these common IRS compliance pitfalls to stay on the right side of the rules.

Overvaluing Donations

One of the most frequent errors is misinterpreting fair market value (FMV). FMV reflects what a willing buyer would pay a willing seller in today's market, not the replacement cost or insured value of the item. This misunderstanding can lead to inflated deductions.

"The FMV of the jewelry is not the value an appraiser determined in an appraisal you obtained so that your insurance company would reimburse you... It reflects only the replacement cost." - IRS Publication 561 [2]

Overstating FMV can result in steep penalties. Claims exceeding 150% of the correct FMV may incur a 20% penalty, while claims at 200% or more can lead to a 40% penalty [2]. If you donate similar items throughout the year and their combined FMV surpasses $5,000, you'll need a qualified appraisal and must complete Form 8283 Section B [6].

Missing Required Documentation

Incomplete or missing paperwork is a surefire way to lose out on legitimate deductions. A case in point: In July 2025, the Tax Court ruled against a taxpayer in John Henry Besaw v. Commissioner (T.C. Summary Opinion 2025-7), denying a $6,760 non-cash deduction for 2019. While the court believed the donations were made, the receipts lacked item descriptions, and Form 8283 was incomplete [10].

"None of the receipts he provided from the charitable organizations included any descriptions of the donated items. This failure alone was fatal to the deduction." - Tax Court Summary Opinion 2025-7 [10]

Besaw's attempt to submit reconstructed records years later was dismissed because they were not contemporaneous [10]. To avoid this, make sure every receipt includes a detailed description of the donated items before leaving the donation site. A receipt with blank fields is essentially useless.

For donations over $5,000, double-check that Form 8283 Section B includes both the qualified appraiser's signature (Part IV) and the donee organization's signature (Part V). Missing either one can result in a denied deduction [6]. Thorough and accurate documentation is your best defense against IRS penalties and ensures your deductions are properly recognized.

How Deductible.me Simplifies Non-Cash Donation Management

Navigating IRS rules for non-cash donations can feel like a juggling act - accurate item valuations, organized receipts, and properly completed forms are all essential. Deductible.me takes care of the heavy lifting, so you can focus on the act of giving without worrying about the paperwork.

AI-Powered Item Valuation and Receipt Management

One of the hardest parts of managing non-cash donations is determining fair market value (FMV). Deductible.me uses AI to assign FMV automatically, based on item condition (Fair, Good, Very Good, or Like New) in line with IRS guidelines. This eliminates the guesswork that could lead to overvaluation penalties.

All your receipts are stored in one centralized, audit-ready system. This not only keeps you organized but also ensures you're prepared for tax season while staying compliant with IRS rules.

IRS-Compliant Reporting with Form 8283 Support

If your total non-cash donations for the year exceed $500, you'll need to attach IRS Form 8283 to your tax return [6]. Deductible.me's Premium plan makes this process easier by generating Form 8283-ready reports. It automatically formats your data and includes all the required details for Sections A and B of the form [6][12].

"Optimize your deductions efficiently. Deductible.me simplifies charitable giving documentation." - Deductible.me [11]

This feature integrates seamlessly with your donation records, ensuring smooth and stress-free reporting.

Tracking Your Annual Giving Goals

Accurate valuation and reporting are just part of the equation. To stay tax-efficient, you also need to track your contributions against IRS limits, which typically range from 20% to 60% of your adjusted gross income (AGI) [6]. Deductible.me helps you stay on top of your giving goals with tools that monitor your annual contributions.

The Free plan supports up to $500 in tracked donation value, while the Premium plan, priced at just $2 per month, offers unlimited tracking, advanced analytics, and priority support. With these tools, you can give strategically without exceeding IRS limits, making it easier to maximize the impact of your donations.

Conclusion

Navigating IRS rules for non-cash donations can feel complex, but the basics are straightforward: donate to a qualified organization, determine the fair market value, ensure items are in good used condition, and keep detailed records. By following these steps, you can make the most of your generosity while staying on the right side of tax regulations.

The IRS enforces strict penalties for errors: a 20% penalty for substantial valuation misstatements, a 40% penalty for gross errors, denial of deductions if a $250+ acknowledgment is missing, and the requirement to file Form 8283 for donations exceeding $500 [2][5][1].

These penalties highlight the importance of thorough documentation. Good records - like photos, written acknowledgments, and accurate valuations - aren’t just helpful; they’re essential. Proper record-keeping can mean the difference between a smooth tax season and an audit headache.

For a simpler way to manage all this, Deductible.me offers a centralized solution. With AI-powered fair market value estimates, Form 8283-ready reports, and an easy system for organizing receipts, it takes care of the compliance work for you. The Free plan covers up to $500 in tracked donations, while the Premium plan offers unlimited tracking and advanced tools for just $2/month.

FAQs

How do I prove fair market value for donated items?

When determining the fair market value of donated items, focus on a few key factors: comparable sales, recent transaction prices, the item's condition, and current market demand. If you're dealing with high-value items, you might need a qualified appraisal to back up your valuation. It's also essential to keep supporting documents like receipts, appraisals, or proof of sale. These records will help substantiate your valuation and ensure you stay in line with IRS guidelines.

When do I need an appraisal for non-cash donations?

If you're donating non-cash items valued at over $5,000, you'll need an appraisal to back up the deduction. For a single piece of clothing or household item that's not in good condition, an appraisal is also required if its value is more than $500. Don't forget to include Form 8283 with your tax return to ensure your deduction aligns with IRS requirements.

What if I get something in return for my donation?

If you donate and receive something in return - like merchandise or tickets - you can only deduct the portion of your donation that exceeds the fair market value of the item or service you received. For example, if what you receive is worth more than $75, the charity is required to provide a written statement. This statement must outline the fair market value of the benefit and the amount of your donation that is tax-deductible.